Author

Mortgages with a high loan-to-value can enable borrowers with small deposits to get a foot on the property ladder.

Loan-to-value is essentially the ratio between the value of the loan you take out and the value of your home. So, if your house is worth £300,000 and you have a £60,000 deposit, your loan-to-value is 80%.

Usually, it’s possible to get mortgages with loan-to-values of between 60% and 100%, however, recent months have seen several mortgage lenders withdrawing high loan-to-value mortgages from the market.

Figures reported by FT Adviser show the number of mortgage deals with a loan-to-value of 90% or above plummeted by 94% over the year to September 2020. The reason, according to Rachel Springall of Moneyfacts, is the high level of demand lenders are experiencing following the pause on house purchases in spring’s lockdown.

If you’re a first-time buyer with a small deposit, or a homeowner looking to remortgage at a high LTV, here’s what you need to know.

There’s much less choice for borrowers

The dramatic drop in the number of high loan-to-value mortgages means borrowers have much less choice than they did previously.

According to Moneyfacts, in October there were just 12 deals at 95% loan-to-value and 51 deals at 90% loan-to-value. Many lenders now offer a maximum loan-to-value of 85%.

In effect, this means if you want lots of deals to choose from, you need a bigger deposit. Data from the Land Registry shows the average house price in the UK is £239,196 as of August 2020. So, to qualify for a mortgage with an 85% loan-to-value, you’d need a deposit of at least £35,880.

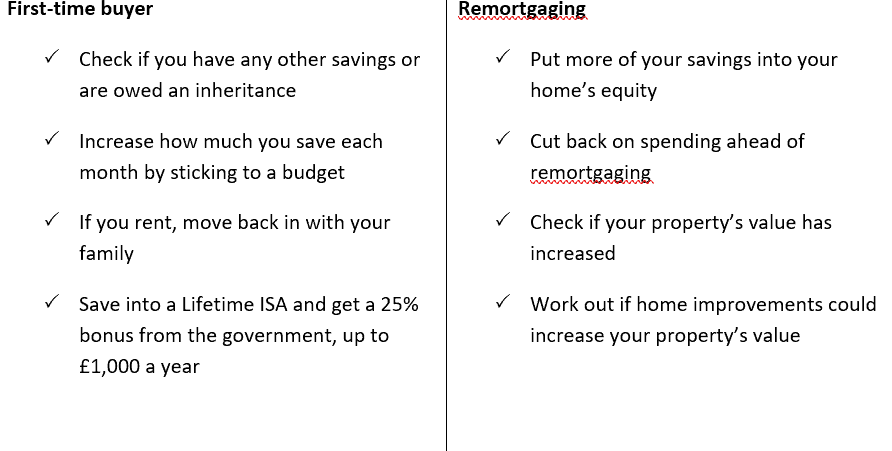

Depending on whether you’re a first-time buyer or remortgaging, there are a few steps that may help you increase your deposit and lower your LTV band.

You could face higher interest rates

If increasing your deposit isn’t an option, you may have to pay a higher interest rate than you would have previously.

It has generally been the case that the higher your loan-to-value, the higher the interest rate. This is because lenders typically view you as a riskier borrower.

The uncertainty caused by the coronavirus pandemic has caused lenders to increase rates on high LTV mortgages even further. Data from Moneyfacts shows the average rate on a two-year fixed-rate deal at 90% LTV was 2.57% on 1 March. This rose to 2.9% on 1 July and increased again to 3.07% on 1 August.

“This would mean someone purchasing a £200,000 property with a 10% deposit on a 25-year mortgage at the average rate would have seen their monthly repayments increase by £46.28 between March and August,” Moneyfacts said. “Over the two-year mortgage term, this would be an extra £1,110.72 in repayments.”

It’s really important to ensure you can afford your mortgage repayments, especially if you’re worried about the impact of the pandemic on your household income.

There are other options available

If the size of your deposit means you’re unable to secure a standard mortgage product, there are other options to consider. Some lenders offer 100% LTV products, although they’re usually guarantor or ‘family assist’ deals.

A guarantor mortgage is when your parent, relative or close friend guarantees to cover your mortgage repayments if you’re unable to pay them. Usually, the guarantor must use their own home as security, which means that if neither of you can afford the repayments, both of your homes could be forcibly sold by the lender. These extra risks mean that getting legal and mortgage advice is crucial.

A ‘family assist’ deal enables one of your family members to act as a guarantor by paying 20-25% of the deposit into a savings account. Once you’ve reached a specified loan-to-value on your mortgage, your family member can withdraw their money. Some family assist deals also use your family member’s property as security.

A financial adviser can help

If you’re a first-time buyer with a small deposit or want to remortgage at a high LTV, speak to a mortgage adviser. They’ll be able to advise you on what type of mortgage is suitable for your needs and what level of repayments you could afford. They’ll also assess whether you could qualify for a lower LTV band.

Specialist mortgage advisers often have access to specialist deals that aren’t available to borrowers directly, so by getting advice you’ll increase your chances of securing the right deal at a competitive rate.

Get in touch

If you’d like advice on buying a home or remortgaging, please don’t hesitate to get in touch. Email us at office@verve-financial.com or call 0330 320 5048.

Please note

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.