Author

The start of a new year is a great time to commit to paying off debts and starting to save for your future.

But this isn’t always as straightforward as it may seem. If you have several debts, it can be difficult to decide which ones to pay off first. You might also be confused about what to put at the top of your to-do list: paying off debts or saving money.

The right way to approach debts and savings will depend on your own financial circumstances and goals. To help you get started, here are some things to think about.

Pay off expensive debts first

If your priority is paying off debts, it’s usually better to tackle the ones with the highest interest rates first. This is because the higher the rate, the more it will cost you in the long run.

Research by Moneyfacts shows the average interest rate on credit cards reached a record high of 25.5% in June 2020. Using the Uswitch credit card interest calculator, if your card balance is £3,000 and you repay £100 every month, you’d pay back a total of £4,499 including interest. But if you increase your monthly repayments to £300, you’d pay back a total of £3,362 – that’s a saving of £1,137.

Other forms of debt that often have high interest rates include personal loans, bank overdrafts and payday loans.

Debts usually cost more than savings

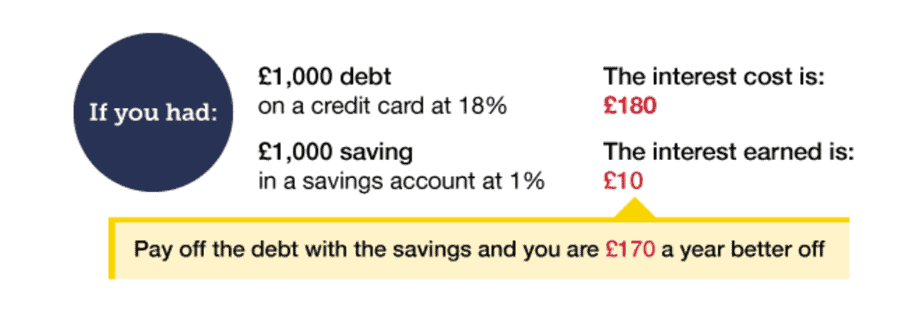

You might be eager to start saving for your future but, in most cases, it will cost you more to borrow than you can earn by saving.

This example from MoneySavingExpert demonstrates why paying off your debts will usually make you better off:

Source: MoneySavingExpert

There are some exceptions. If you have a fixed-rate loan that charges a penalty for paying it off early, then it might be better to save your money instead.

In addition, if the interest rate on your debt is less than the rate on your savings account, you might be in a stronger position by building up savings.

Tread carefully when making mortgage overpayments

Overpaying on your mortgage could put you on a stronger financial footing. You’ll be able to pay off your mortgage quicker and pay less interest overall.

Mortgage interest rates are currently higher than savings accounts interest rates. Data from Moneyfacts shows that in November 2020, the average two-year fixed-rate on a 75% loan-to-value was 2.27%, whereas the average five-year fixed-rate was 2.51%.

For savings accounts, the highest two-year fixed rate was 0.93% and the highest five-year fixed rate was 1.25%, according to MoneySavingExpert data collected on 11 December.

Before you make a mortgage overpayment, it’s important to check your lender’s terms and conditions.

Lenders usually let you overpay the equivalent of 10% of your mortgage balance each year, although this varies from one lender to another. If you overpay by more than this, you could face an Early Repayment Charge, which may range from 1% to 5% of the amount overpaid.

Build up an emergency fund

Sometimes, life doesn’t go as smoothly as we hope. A period of unemployment, a broken boiler or a leaking roof could happen when you least expect it. If you haven’t prepared in advance, there’s a risk you’ll end up in financial difficulty.

Building up an emergency fund is crucial to ensure you can pay for life’s unexpected events. So, before making a large mortgage overpayment, make sure you have enough cash to see you through bad times.

In general, you should keep around six months’ worth of regular outgoings in an easily accessible savings account.

Start saving into a pension

Once you’ve paid off expensive debts, it’s a good idea to start planning for your future. You might be tempted to put all your extra cash into paying off your mortgage, however, saving money into a pension could be a great way of building your future financial resilience.

It isn’t possible to compare mortgage interest rates with pension interest rates because the latter doesn’t exist. Money in a pension is invested across a range of different assets, including shares, and their value goes up and down. You must be comfortable taking on investment risk.

A big benefit of saving into a pension is the government adds 20% tax relief to your contributions. This effectively means a £1,000 pension contribution only costs you £800. If you’re a higher-rate or additional-rate taxpayer, you can claim a further 20% and 25%, respectively.

If you’re employed, you’ll also benefit from employer contributions into your pension.

Speak to a financial adviser

The right solution for you will depend on various factors, including your financial circumstances, your goals, and your attitude to debt and savings.

A financial adviser can help you determine the right way forward. They will:

- Show the impact of paying off various debts

- Make sure you’re on the right mortgage deal

- Look out for any Early Repayment Charges or penalties

- Help you define your financial and life goals

- Run through a range of scenarios to show the effect of paying off your mortgage versus saving into a pension.

Get in touch

If you’d like advice on structuring your finances, finding the right mortgage and saving for your future, we can help. Please email us at office@verve-financial.com or call 0330 320 5048.

Please note

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future results.