Teaching your children about money is an indispensable life lesson that will boost their chances of a financially secure adulthood.

The thought of explaining saving and budgeting to a bored pre-schooler or grumpy teenager might fill you with dread. However, there are lots of ways of making finance interesting, no matter how old your children are.

From toys to smartphone apps, read on to discover some age-appropriate ways to teach your children about money.

Play maths games with your toddler

Before your child can begin to understand money, they need some basic maths skills.

Toddlers can typically start reciting numbers from around 18 months of age. Between the ages of two and three, they’ll usually grasp the concept of ‘how many’ and be able to count objects.

You can start to introduce addition and subtraction before your child starts school. Some fun ways to do this include adding and removing teddy bears at a teddy bears’ picnic; making taller and shorter block towers; and adding and taking away chocolate buttons (warning – they’ll probably eat a lot of them!).

Playing shops is a fun way to teach the concept of value and improve your child’s numeracy skills. There are some simple online numeracy games on the CBeebies website, featuring much-loved characters like Peter Rabbit and Postman Pat.

Introduce pocket money from age four or five

The sooner your children become familiar with money, the quicker they’ll be able to appreciate its value. This is really important for building healthy spending habits.

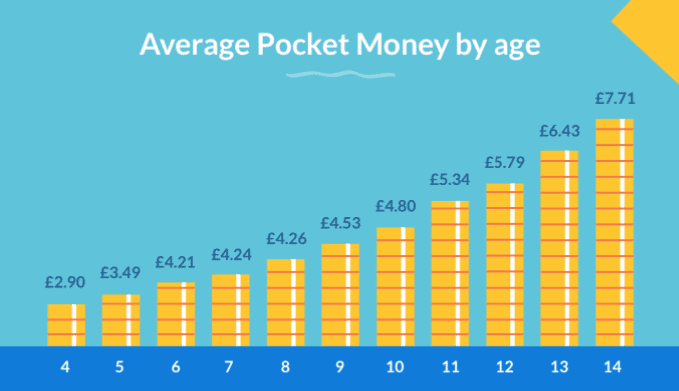

According to the Money Advice Service, a child’s money habits have largely formed by the age of seven, so it may be worth introducing pocket money when they’re four- or five-years-old.

Research by Rooster Money suggests the average amount of pocket money given to a four-year-old is £2.90 a week.

Source: Rooster Money

A piggy bank in the form of a see-through jar will enable your child to clearly see their money building up. Your child could even have two jars – one for spending and one for saving.

Pay for chores

Paying your child for completing chores will help them to understand that money must be earned. Chores could include anything from emptying the dishwasher to cleaning the car or weeding the garden.

You could even set weekly chores that your child must complete before they receive their pocket money.

If you never have cash to hand, a pocket money app like Rooster Money or gohenry might help. Both let you transfer pocket money and set spending limits and targets. When they’re older, your child can get a linked prepaid debit card.

Encourage your child to save

Encouraging your child to save money is a great way of instilling financial discipline.

Some banks and building societies let children open a savings account from age seven. This will help your child begin to understand interest, deposits and withdrawals.

One way of supporting saving is to match your child’s contributions. For young children, this could be pound for pound; for older children, 50p or 25p for each pound might be more reasonable.

There are lots of online resources and apps that can help children learn about saving. For example, the app Gimi combines a pocket money and chores manager with financial education. There are three lessons on earning, saving and spending that you and your child can work through together.

Introduce older children to investing

As your children get older, you can start to teach them about investing.

One way of doing this is to open a Stocks and Shares Junior ISA. In the 2020/21 tax year, you can invest £9,000 a year into a Junior ISA. Your child can’t touch the money until they reach age 18.

As well as building up money for your child’s future, you can use a Junior ISA as a way of explaining how the stock market works.

Your teenager might enjoy playing the online game Piggybank Fantasy Stock Exchange. Supported by the London Stock Exchange, each user gets £100 of Piggybank cash and ten free shares. Your child chooses which companies they’d like to invest in and, if they’re successful, there’s a chance of winning a £250 gift voucher.

Get in touch

If you’d like advice on saving and investing for your children, please email us at office@verve-financial.com or call 0330 320 5048.

Please note:

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.