Author

If your children are struggling to get a foot onto the housing ladder, you might be thinking about lending a helping hand.

You’re certainly not alone. According to Legal & General and Cebr, the so-called ‘Bank of Mum and Dad’ is expected to back nearly one in four (23%) housing transactions in 2020, providing a total of £3.5 billion.

The report found that, on average, the Bank of Mum and Dad gifts £20,000 to help family or friends buy a home.

Before you part with your hard-earned cash, it’s important to understand the financial and legal consequences. Here are three things to think about.

1. Supporting your children could affect your own financial security

As a parent, it’s natural to want to help your children, especially when they reach the exciting stage of buying their first home.

However, you also need to think about your own financial security. Can you really afford to part with thousands, or tens of thousands, of pounds? Even if you feel financially secure now, what could your finances look like in 20- or 30-years’ time?

It’s important to think carefully about how much you can realistically give to your children. If handing over money means you can’t enjoy your day-to-day life or cover unexpected emergencies, then it probably isn’t viable.

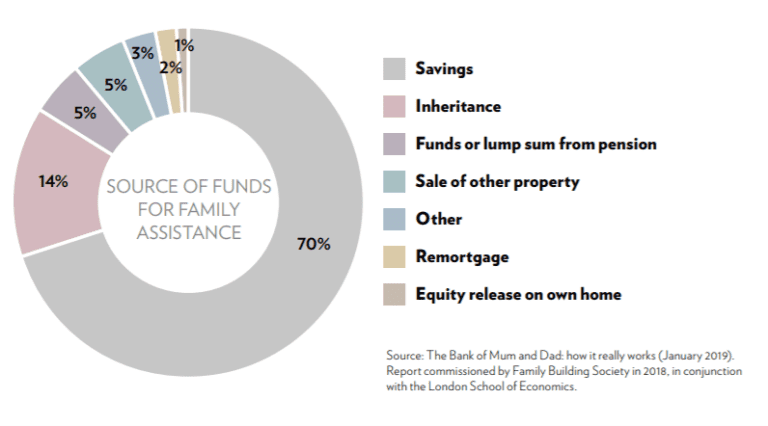

A 2019 report by The Family Building Society shows some parents have resorted to taking money out of their pension to help their children buy a house, with 5% of the total money coming from funds or a pension lump sum.

The effect of raiding your pension pot shouldn’t be underestimated. There’s a real risk you won’t have enough income to live a comfortable retirement. Worse, you could run out of money.

Remember, your financial wellbeing is just as important as your children’s.

2. Transactions and arrangements should be documented

Life doesn’t always turn out the way we hope it will. When you’re parting with a large sum of money, it’s vital to plan for unexpected events.

Your child might be buying a home with a partner who they have a seemingly perfect relationship with. Sadly, even the most blissful of relationships can break down. Without proper legal documentation in place, your child’s ex could disappear with half your money.

To protect against this, you need to have clear evidence of your intention behind the money, including whether it’s a gift or a loan, and whether it’s just for your child’s benefit or for them and their partner.

Drawing up a ‘declaration of trust’ is one way of documenting where money has come from and what impact it has on the ownership of the property.

Bear in mind, things can become even more complicated if two sets of parents are contributing to the house deposit. Drawing up an agreement will help to prevent disputes if one set of parents suddenly needs their money back.

3. Beware the tax implications

Although neither you nor your child will have to pay immediate tax on gifted money, your estate could be liable for Inheritance Tax (IHT) further down the road.

In the 2020/21 tax year, you can give away £3,000 worth of gifts without them being added to the value of your estate. You can carry any unused annual exemption forward by one year. So, in total, two parents might be able to gift £12,000 without having to worry about IHT.

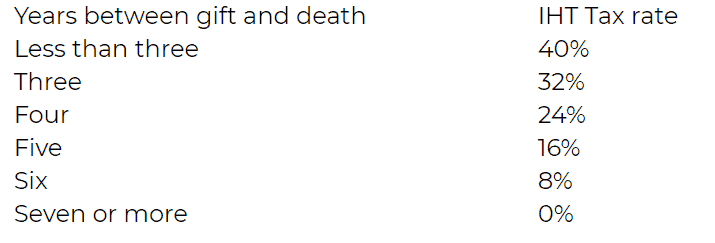

If you give more than this and you die within seven years, the money will form part of your estate when working out your IHT liability. If your total estate is worth more than £325,000, tax of up to 40% would be due on the excess.

Source: HomeOwners Alliance

Another tax to watch out for is Stamp Duty. Some parents help their child buy a home by taking out a joint mortgage with them. However, if you already own a property, your child’s house will count as a second home and attract an additional 3% Stamp Duty. You might also have to pay Capital Gains Tax when the property is sold.

One way of legitimately escaping these tax traps is to take out a ‘Joint Borrower, Sole Proprietor’ mortgage. This enables parents to be a mortgage borrower without being named on the title of the property.

Get in touch

There are lots of pros and cons to becoming the Bank of Mum and Dad. By assessing the health of your finances and explaining the potential pitfalls, we can help you to decide whether it’s right for you.

To find out more, email us at office@verve-financial.com or call 0330 320 5048.

Please note

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.