Christmas is the season of spending time with loved ones, cuddling up in front of a festive film, and eating too many mince pies.

It’s also the season of many, many presents. Christmas can come with a hefty price tag which, if you don’t plan carefully, could cause a major dent in your finances.

To ensure the festive season doesn’t cause you financial misery, here are the dos and don’ts of Christmas spending.

Don’t: Spend more money than you have

The first Christmas no-no is spending more money than you actually have.

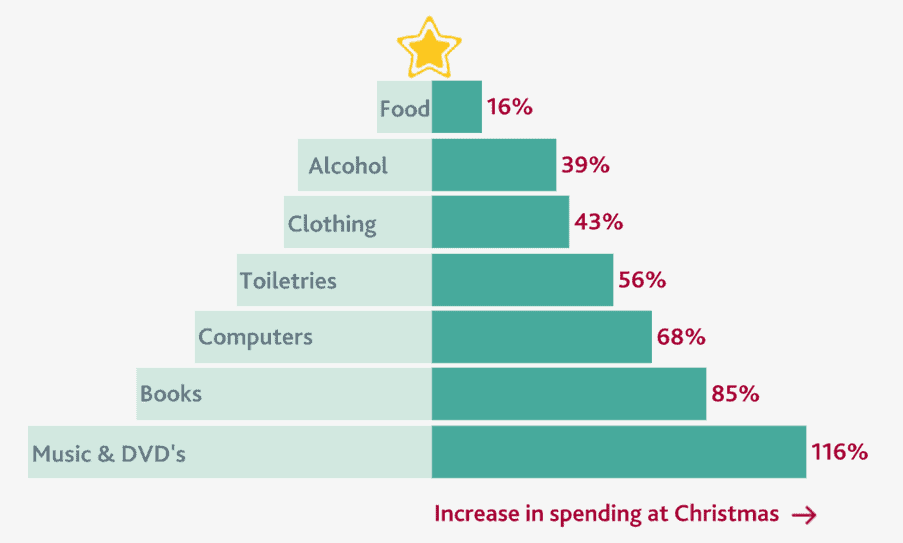

According to the Bank of England, the typical UK household spends around £2,500 each month. But in the run-up to Christmas, people’s spending habits change dramatically.

The average household spends £800 more in December compared with other months. As well as buying gifts for friends and family, people tend to spend more on things like food, alcohol and clothes.

Source: Bank of England

There’s a risk that if you spend more money than you have, you’ll rack up expensive debts and overdrafts. You’ll also be saving less money, meaning your financial goals could go off track.

Do: Set a budget

To avoid spending more money than you have, it’s a good idea to set a Christmas spending budget.

Start by making a list of all the people you’re buying presents for and all the other Christmassy things you plan to buy. Next, work out how much you can afford to spend based on your available income.

The Money Advice Service has created a Christmas Money Planner, which can help with this task.

You enter how much money you have, what you’re able to save between now and Christmas, and what you plan to spend on presents, food and drink, decorations, travel, going out, and clothes. It calculates how much money you’re likely to have left or how much you’ll overspend by.

It’s worth creating a budget for the rest of the year, too. By working out the difference between your take-home pay and expenses, you can check whether you’re living within your means. You might spot areas where you’re able to make cutbacks, which could result in more money going towards savings.

Don’t: Go into debt

Sticking to a budget is difficult at the best of times. For many people, this Christmas could be harder than ever because of the financial strain caused by the coronavirus pandemic.

A survey by the Money Advice Service found a third of people are more worried than last year about being able to afford the Christmas they want. A quarter are worried about going into debt.

Using credit cards or loans to pay for Christmas might seem like an easy option. However, the interest could soon rack up. According to MoneySavingExpert’s Loan Calculator, if you take out a £1,000 loan over three years with a 10% interest rate, you’ll end up repaying £1,161.

A better option is to try to cut costs by looking for cheaper or free alternatives. Remember, it’s the thought that counts.

Do: Consider gifting money to children

If you’re tired of buying your children or grandchildren expensive gifts that they soon grow bored of, why not consider gifting money instead?

One option is to open a Junior ISA. There are two options: a Cash Junior ISA, which pays interest, or a Stocks and Shares Junior ISA, where the money is invested in the stock market.

Your child can’t access the money until they turn 18, so it could prove a useful way of boosting their financial security in adulthood.

The maximum amount you can pay into a Junior ISA in the 2020/21 tax year is £9,000.

Don’t: Forget about your financial goals

It’s easy to get carried away at Christmas and forget about the bigger picture. But overlooking the impact of Christmas spending on your finances could derail your goals.

If you’ve been diligently saving money each month – perhaps to buy a house, pay for university fees or fund your retirement – it’s worth trying to stick to your saving habits in December.

An extra £500 here or there might not sound like much, but in the long run, it could make a big difference. The savings calculator from This is Money shows that if you invested £800 for 15 years with an annual interest rate of 4%, your money could grow to £1,456. That’s potentially an extra £656 going towards your financial future.

Don’t forget, the money you save into a pension benefits from 20% tax relief, so a £1,000 contribution only costs you £800.

Get in touch

If you’d like advice on your finances, please get in touch. Email office@verve-financial.com or call 0330 320 5048.

Please note:

The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.