The economic crisis caused by the coronavirus and the subsequent lockdowns have had a significant effect on many people. As a result, millions of people have cut back their pension contributions as they feel a squeeze on their household finances.

However, while it might be tempting to cut back on your pension contributions to have more money in the short term, it can have a significant impact on your finances and quality of life in the long term. Read on to find out why you shouldn’t let the pandemic affect your pension contributions.

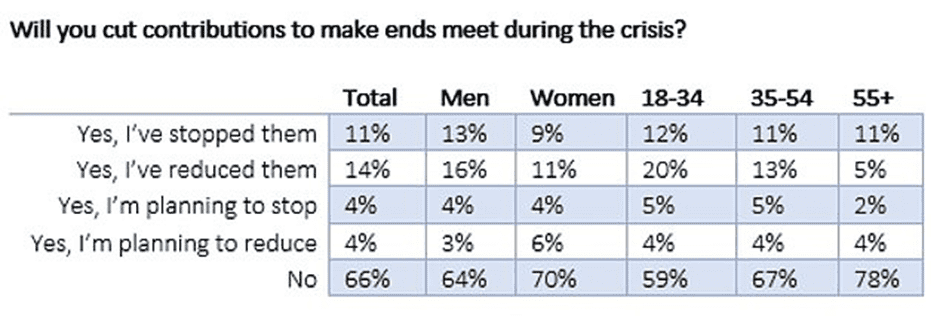

Around 9 million Brits have had to borrow just to make ends meet in recent months

In recent months, the coronavirus pandemic and the subsequent lockdowns have meant that many families in the UK have had to tighten their belts.

Whilst the government’s introduction of the furlough scheme has supported millions of workers who have been unable to work due to the lockdowns, many Brits have struggled to get by. According to figures from the Office for National Statistics (ONS), published by the BBC, around nine million Brits have had to increase their borrowing in recent months just to pay for essentials.

The financial impact of the pandemic has caused many people to reduce their pension contributions, without fully considering the consequences of this decision.

According to a recent study by pension firm Hargreaves Lansdown, published in the Telegraph, a quarter of Brits have either reduced their monthly contributions or stopped contributing entirely. On top of this, a further 8% stated that they planned to do so in future.

Source: This is Money

As you can see, the people who are most likely to reduce or halt their pension contributions are young adults. This may be understandable, as they’re more likely to have a lower salary and thus be more vulnerable to financial shocks.

However, the younger you are, the more of an impact a reduction in contributions can have on your pension fund by the time you come to retire. The reason for this is the incredible effect of compound interest.

Young people are more affected by halts in contributions due to compound interest

Albert Einstein once referred to compound interest as the “eighth wonder of the world” because of how significant its effects can be.

When you’re saving for your retirement, most financial planners will typically recommend that you start as soon as possible.

One of the reasons for this is obviously that starting earlier will give you longer to make contributions, but another reason is that your contributions will compound over time.

This means that you won’t just benefit from the returns on your pension contributions, but also on the growth on these returns.

Due to the effect of compound interest over a long period of time, young people can be significantly affected if they reduce their pension contributions. This is because even a small amount can become much larger if left to accrue compound returns for several decades.

A recent report by financial services provider Aegon has calculated the impact that even small reductions in pension contributions can make.

According to the report, if the average 25-year-old took a break in pension contributions for just three years, it would reduce their pension fund by £15,500 by the time they retire.

Furthermore, an annual reduction of only 1% until State Pension Age would leave them with a shortfall of £18,400.

Halting your pension contributions will mean you lose your employer’s workplace contribution

Another reason not to reduce your pension contributions is that, if you are enrolled in a workplace pension, you may lose your employer’s contributions too.

Since 2012, all employers automatically enrol their employees into a workplace pension, unless they specifically opt out. The minimum contribution in such schemes is typically 5% of your salary but this is topped up by a further 3% by your employer.

This means that if you were to halt your contributions by opting out of a workplace pension, you are not just losing your own contribution but also that of your employer.

Using the workplace pension contribution calculator from the Money Advice Service, we can work out how much you may stand to lose.

For example, if you had a salary of £24,000 per year, then your average qualifying earnings for working out your pension contributions would be £17,760. This is your pre-tax salary minus the lower earnings threshold of £6,240.

With this level of qualifying earnings, your pension contributions each year would be £888, while your employer would pay in an additional £532.80. If you were to halt your pension contributions, you would also lose this amount from your employer.

Even if this employer contribution does not seem high compared to your own contribution, every little helps. Furthermore, as we mentioned earlier, the effects of compound interest on your employer’s contribution can add up to a significant amount in the long term.

If you struggle to make ends meet, cutting back on your pension contributions should be one of the last things you consider, as it can have a significant impact on your finances in retirement.

Instead, you may benefit from speaking to a financial adviser, who can help you to reorganise your finances to help you to meet your financial goals without having to sacrifice future comfort for current convenience.

Get in touch

If you need help reorganising your finances so you don’t need to reduce your pension contributions, we can help. Email us at office@verve-financial.com or call 0330 320 5048.

Please note:

A pension is a long-term investment. The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

Workplace pensions are regulated by The Pension Regulator.

Tax treatment varies according to individual circumstances and is subject to change.